Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM reported on July 14:

In the first half of 2025 (H1), all segments of the sodium-ion battery industry chain showed significant growth. However, the industry is facing a critical turning point amid technological route changes, cost pressures, and market challenges.

I. Cathode Materials: Structural Innovation and Price Competition

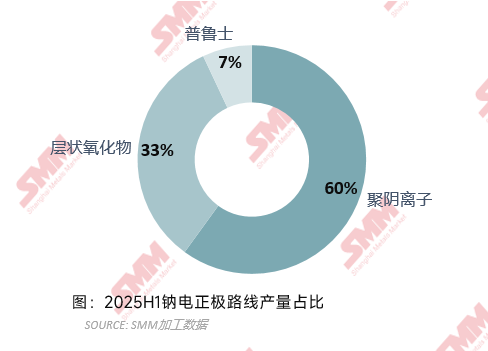

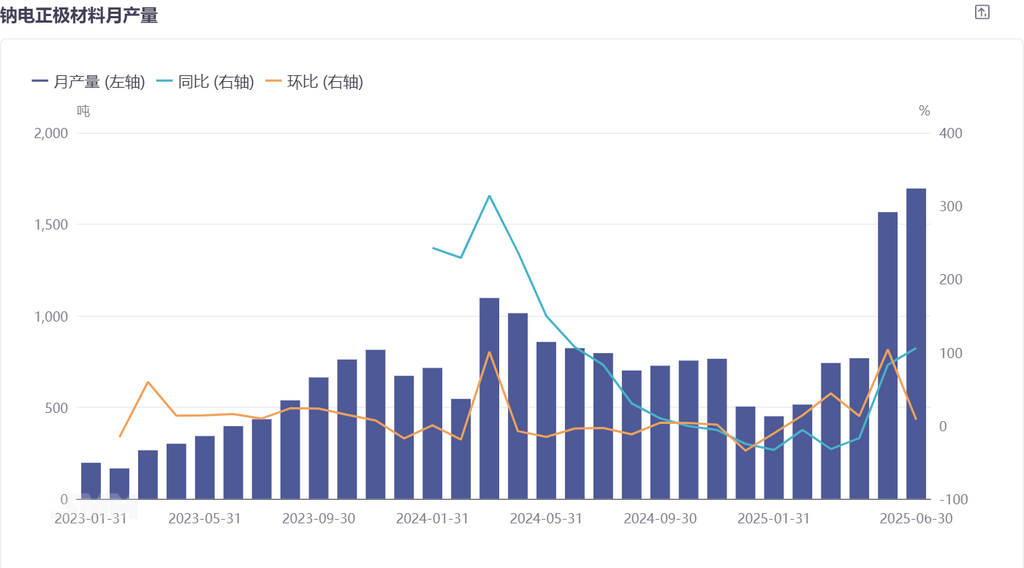

In the first half of 2025, the sodium-ion battery cathode material market exhibited dual characteristics of technological route differentiation and intensified cost competition. Total cathode material production from January to June increased by 14% YoY. Among them, the polyanion route (mainly NFPP) became the absolute mainstream with a 60% market share, while the layered oxide route's share declined to 33%, and the Prussian blue route maintained a niche position at 7%.

The explosive growth of the polyanion route was the biggest highlight in the first half. NFPP production in Q2 surged by 400% MoM, driven by the concentrated commissioning of enterprise-level 10,000 mt production lines. The scale effect significantly reduced costs. SMM data showed that the average price of NFPP in June dropped nearly 30% from the beginning of the year, approaching the 25,000 yuan/mt threshold.

The layered oxide route faced strategic challenges. Squeezed by NFPP, downstream battery cell manufacturers accelerated the switch to other technological routes, leading to a YoY decline in layered oxide demand exceeding 20%. To compete for market share, enterprises were forced to initiate a price war. The average price of SMM's layered oxide O3 cathode in June dropped by 16% from January, with some enterprises even taking orders below cost. Notably, the Institute of Physics, Chinese Academy of Sciences successfully suppressed P2-O2 phase transitions and activated oxygen/manganese synergistic redox through anti-site structural design (Li/Mn self-locking structure), improving the cycle life of layered oxides to 159.6 mAh/g (20 cycles), preserving the technological potential of this route.

The Prussian blue route explored differentiated breakthroughs. Despite remaining niche, this route stood out in specialized scenarios due to its low cost and excellent rate performance.

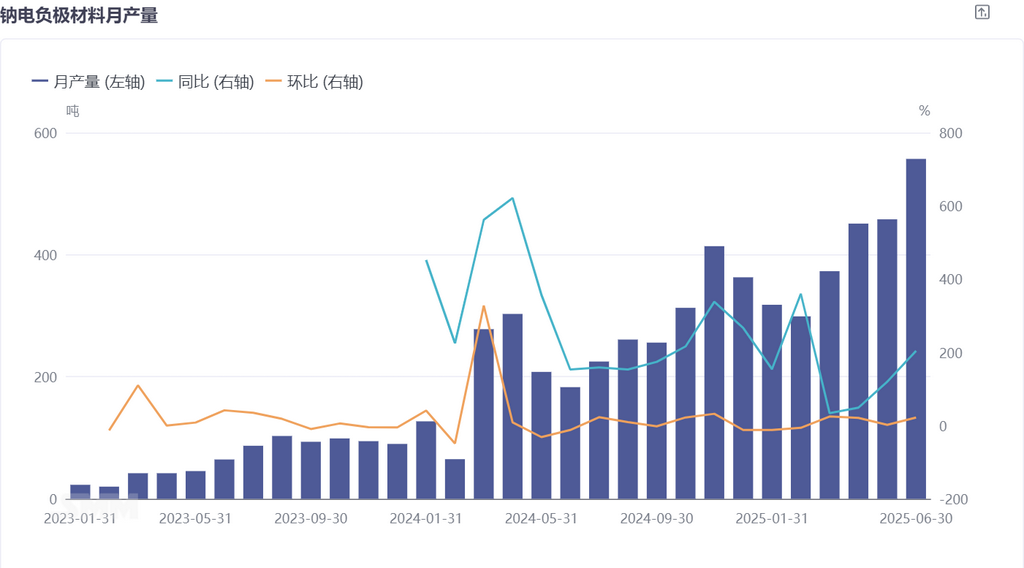

II. Anode Materials: Biomass Coconut Shell Charcoal Dependency and Cost Breakthroughs

Hard carbon anodes continued to show strong growth momentum, with production from January to June increasing by 47% YoY. Among them, biomass-based hard carbon accounted for 85%, with coconut shell charcoal remaining the main raw material. However, since Q2, the import price of Indonesian coconut shell charcoal has continued to rise, increasing by 20% from the beginning of the year, creating a sharp contradiction with the sodium-ion battery's cost reduction needs. Enterprises accelerated the shift to low-cost alternative solutions:

Fossil fuel-based hard carbon R&D accelerated: Guoke Carbon America's hard carbon product prepared from coal-based pitch has a specific capacity exceeding 300 mAh/g, a compaction density of 1.0 g/cm³, raw material costs only one-third of biomass-based, and a production yield exceeding 50%. Top-tier enterprises such as BSG and BTR have initiated the construction of 10,000 mt pitch-based hard carbon production lines.

The industry exhibits a dual-track development pattern, with biomass-based materials maintaining market share and fossil-based materials striving for future growth. It is expected that in the second half of the year, pitch-based hard carbon will penetrate into the ESS and start-stop battery sectors, driving down the prices of anode materials.

III. Electrolyte: Lithium Battery Capacity Integration and Cost Reduction

The production of sodium-ion battery electrolytes increased by 27% YoY, but the industry landscape shows significant dependency characteristics, with 90% of the capacity coming from converted production lines of lithium battery enterprises. Customized requirements dominate product development, with differences exceeding 30% in sodium salt concentration and additive formulations (such as FEC, VC) among different battery cell manufacturers, making it difficult for small and medium-sized producers to achieve large-scale production.

The cost side is characterized by solvent-driven fluctuations and additive-constrained profits. The average price of sodium hexafluorophosphate (NaPF₆) fell by 14% compared to the beginning of the year, driving down the cost of electrolytes. Specialty additives (such as sodium bis(fluorosulfonyl)imide) cost as much as 150,000 yuan/mt, accounting for a significant portion of electrolyte costs and becoming a key factor in cost reduction.

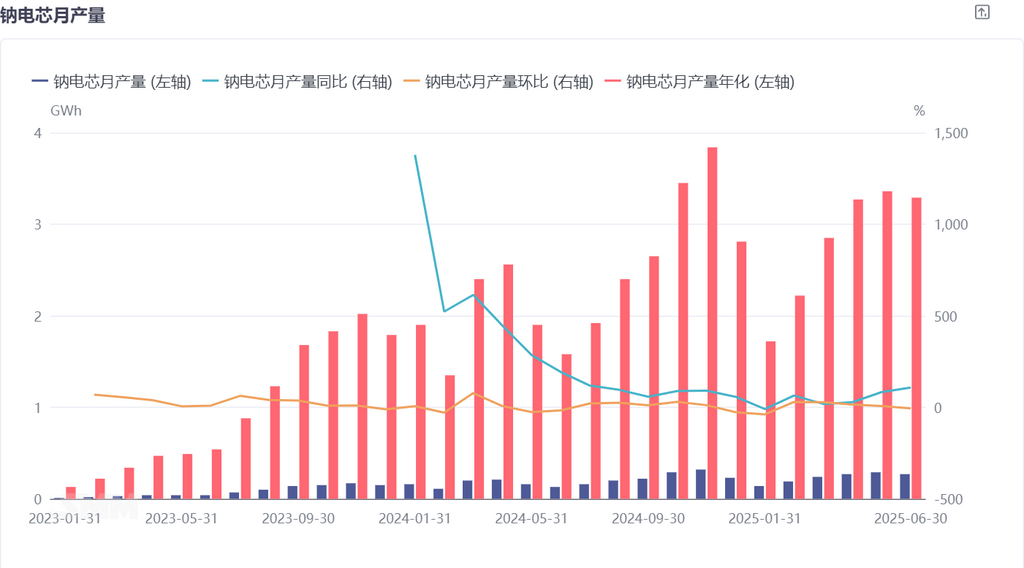

IV. Battery Cell Manufacturing: Shipment Pressures and Scenario Breakthroughs

From January to June, sodium-ion battery cell shipments increased by 44% YoY, but fell short of achieving 50% of the annual 5GWh target, mainly due to delays in ESS project tenders and the lack of momentum in the two-wheeler market. Insufficient price competitiveness remains a core pain point: the current average price of sodium-ion battery cells is 0.5-0.6 yuan/Wh, more than double that of LFP battery cells, with a significant gap in energy density.

Meanwhile, enterprises are accelerating their exploration of differentiated paths (compiled from news media reports):

ESS sector focuses on low-temperature scenarios: BYD's 20MWh sodium-ion battery cube was put into operation in Nanning Industrial Park, maintaining a 90% capacity retention rate at -20℃ and exceeding 6,000 cycles; EAST's 50kW/100kWh industrial and commercial ESS power station uses long-life sodium-ion battery cells, with an annual discharge capacity of 60,000 kWh and a cost per kWh 0.12 yuan lower than that of lithium batteries. The feasibility of sodium-ion batteries in power grid frequency regulation was verified by the National Energy Group's Ningxia Electric Power hybrid ESS project (including 200kW/400kWh sodium-ion batteries).

Breakthroughs in overseas markets: Guangdong Highstar's sodium-ion battery star won a 1GWh overseas order, with products used in European and American household ESS systems, requiring a discharge capacity of ≥85% at -40℃ and a cycle life of ≥6,500 times, marking the certification of Chinese sodium-ion batteries in the high-end market.

Technological innovations push performance boundaries: CATL's "Sodium New" battery achieves an energy density of 175Wh/kg through anode-free technology, supporting 5C ultra-fast charging and cold start at -40℃; Chilwee Group's developed 24V heavy-duty truck start-stop battery cell exceeds 8 years of cycle life, reduces costs by 61% compared to lead-acid batteries, and has been mass-produced for Shaanxi Auto's heavy-duty trucks.

V. Industry Outlook: Technological Iteration and In-depth Exploration of Application Scenarios

In the first half of the year, the sodium-ion battery industry exhibited characteristics such as accelerated reconstruction of the material system, strong momentum in cost reduction, and breakthroughs in application scenarios at different levels. Looking ahead to the second half of the year, three major trends are worth noting:

Continuous decline in material prices: It is expected that the average price of NFPP will fall to around 20,000 yuan/mt, the price of hard carbon anode will continue to decline, and the price of NaPF6 will further approach 50,000-60,000 yuan/mt, driving the cost of sodium-ion battery cells into the 0.4 yuan/Wh range.

ESS becomes the growth engine: The 100MW-level sodium-ion battery ESS projects of central state-owned enterprises such as SPIC and China Huaneng Group will be connected to the grid in a concentrated manner. Coupled with the surge in European household ESS orders, this will drive an increase in sodium-ion battery shipments for ESS in the second half of the year.

The final outcome of technological routes is approaching: The market share of the polyanion route in the sodium-ion battery ESS sector is expected to continue to break through. The layered oxide route is moving towards high-end applications, Prussian blue focuses on special application scenarios, and the hard carbon anode is gradually transitioning from reliance on imports to localisation of raw materials, while accelerating R&D on fossil fuels.

In the first half of 2025, the sodium-ion battery industry chain will experience a comprehensive rise in production. The explosive growth of polyanion cathode materials (especially NFPP) and the increasing volume of hard carbon anode production will be highlights. However, challenges such as raw material cost pressure (e.g., coconut shell charcoal), market compression and price competition faced by layered oxides, and the need to improve the overall cost-effectiveness of sodium-ion battery cells cannot be ignored. In the second half of the year, cost reduction and efficiency improvement in the industry chain (including declining material prices and the development of new raw materials) and battery cell enterprises seeking differentiated technological breakthroughs will be key to determining whether sodium-ion batteries can gain a firm foothold in the fiercely competitive new energy market.

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lv Yanlin 021-20707875

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn